Hedhvick Hirav

Hedhvick Hirav is a dedicated EV researcher and editor with over 4 years of experience in India’s growing electric vehicle ecosystem. Their contributions have been recognized in leading sustainability publications and automotive journals.

Summarize & analyze this article with

Choose an AI assistant and open this article directly:

Tip: if the AI doesn’t fetch the page automatically, paste the article URL manually.

What is an EV EMI Calculator and How Does It Work in India?

When you’re thinking of buying an electric vehicle (EV) in India, you might worry about the upfront cost. That’s where an EV EMI calculator steps in—it helps you estimate your monthly loan payments (EMIs) when purchasing an EV, making the buying process practical and less stressful.

- An EV EMI calculator is an online tool designed to estimate your equated monthly installments (EMIs) for electric vehicles.

- You simply enter the price of the EV, the down payment you plan, the loan tenure, and the current interest rate.

- The calculator will instantly show your monthly EMI, the total interest outgo, and the full repayment amount.

- This helps you decide whether your new EV fits your personal budget.

EV EMI calculators are now available across all Indian banks’ websites, major non-banking finance companies (NBFCs), and auto manufacturer portals, tailored specifically for electric cars, bikes, and three-wheelers.

- You can compare multiple options side-by-side, since rates, processing fees, and offers vary.

- For well-known brands (like Tata, MG, Mahindra, and Ola Electric), many calculators also show special EV loan deals valid in 2025.

Did You Know?

RBI data suggests that in 2025, the average interest rate for EV loans in India is lower by 0.5%-1% compared to regular auto loans. This is a direct result of government efforts to boost EV adoption.

Why Should You Use an EV EMI Calculator Before Buying an Electric Vehicle?

You may wonder: Isn’t it better to talk directly to your bank or NBFC for loan options? Actually, using an EV EMI calculator first gives you the upper hand:

- You know your EMI before you even visit the dealership or speak to a loan officer.

- You can adjust your down payment or loan term in seconds to see what suits you best.

- There are no hidden costs or surprises, since most calculators automatically include processing fees and insurance.

- Calculators use the latest bank interest rates, often updated for 2025 electric vehicle schemes and EV-specific discounts.

- You save time and avoid manual calculations (which can be confusing or error-prone).

Before you sign a loan agreement, having this info helps you negotiate better—sometimes banks offer rate cuts or waive certain charges if you show you’ve researched!

Expert Insight

SEBI consumer research shows that EV buyers who use online EMI calculators are 37% less likely to overspend or skip key costs (insurance, registration, etc.) in their purchase planning.

What Types of Electric Vehicles Can You Calculate EMIs For in India?

Not all EV EMI calculators are limited to electric cars. In 2025, most major lenders and OEMs cover:

- Electric cars (hatchbacks, sedans, SUVs)

- Electric two-wheelers (scooters and motorcycles)

- Electric three-wheelers (passenger and cargo autos)

- Commercial EVs like delivery vans and buses (special EMI calculators may be required)

With rapid adoption in India, these calculators use model-wise prices and tailor interest rates for different categories.

Key Examples

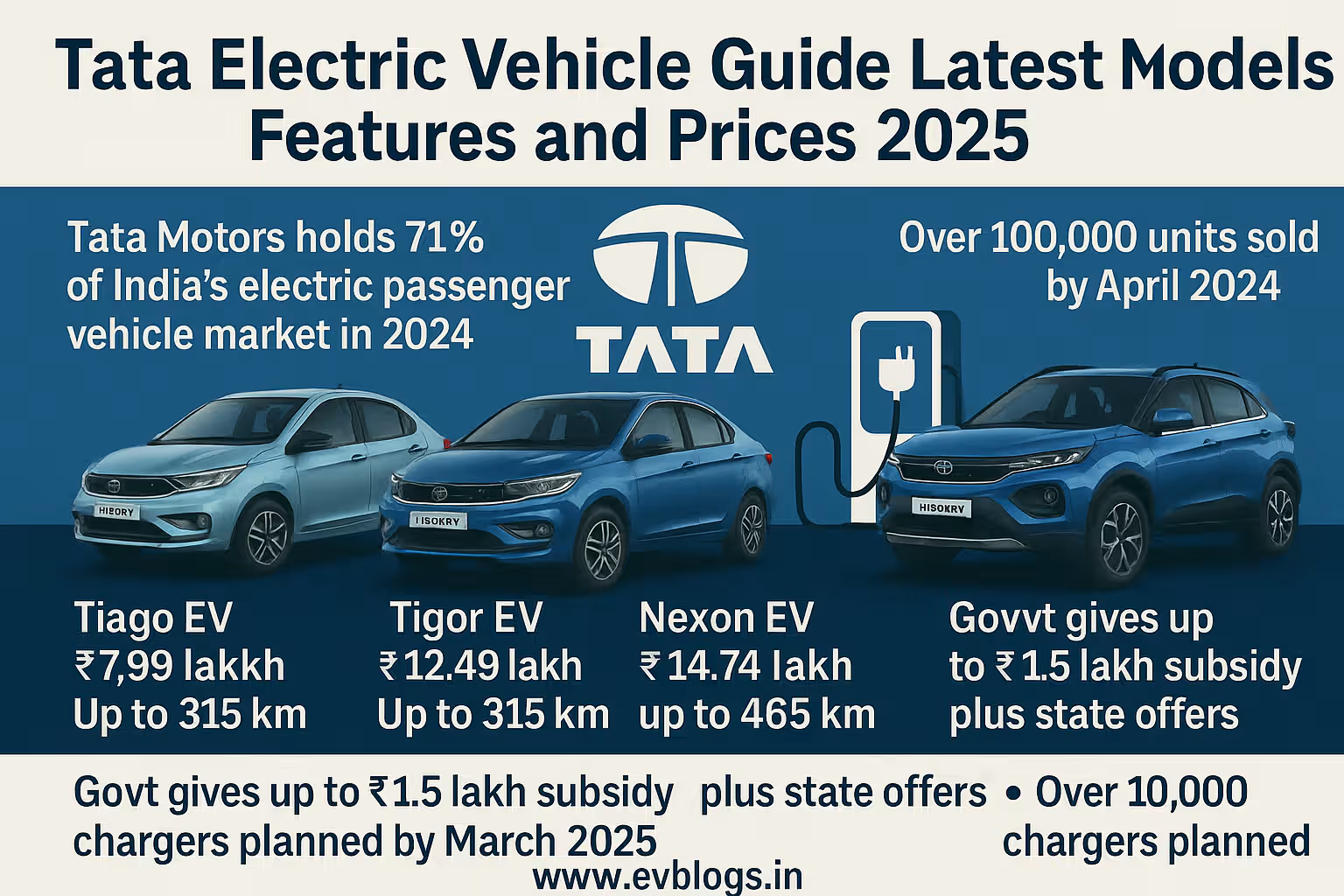

- Tata Tiago EV, Tata Nexon EV (cars)

- MG ZS EV, Mahindra XUV400

- Ather 450X, Ola S1 Pro (two-wheelers)

- Hero Electric Optima, TVS iQube

- Piaggio Ape e-City (three-wheeler)

Did You Know?

According to SIAM, India’s electric two-wheeler market in 2025 will double, and dedicated EMI calculators for EV scooters are now a top feature on dealer and aggregator portals.

Which Are the Top Banks and Lenders Offering Electric Vehicle Loans in 2025?

In 2025, EV loans have become mainstream, with most major banks and NBFCs in India offering EV-specific products. Here’s a comparison of top lenders you can expect to encounter:

| Lender/Bank | Min. Interest Rate (2025) | Max. Loan Tenure | Loan Up to On-Road Price | Processing Fee | Popularity with EV Buyers |

|---|---|---|---|---|---|

| SBI | 8.55% | 7 years | 90% | ₹5000 | Very High |

| HDFC Bank | 8.75% | 7 years | 100% (select EVs) | ₹5000+GST | Very High |

| ICICI Bank | 8.90% | 7 years | 100% | 0.5% of loan | High |

| Axis Bank | 8.60% | 7 years | 90% | ₹3500+GST | High |

| Bank of Baroda | 8.70% | 7 years | 100% | ₹2500 | Medium |

| Punjab National Bank | 8.75% | 7 years | 85% | ₹1500 | Medium |

| Tata Capital | 8.80% | 7 years | 100% | ₹5999 | Very High (Tata EVs) |

| Mahindra Finance | 9.10% | 5 years | 100% | 1% of loan amt | High (Rural areas) |

| IDFC FIRST Bank | 8.95% | 7 years | 90% | ₹3500 | Medium |

| Bajaj Finance | 9.25% | 5 years | 95% | ₹4000 | High (Two-wheelers) |

How to Pick the Right Lender

- Check the maximum percentage of vehicle price funded (some banks offer 100% on-road price).

- Compare effective interest rates; even 0.5% makes a visible difference in total outgo.

- Choose lower processing fees, and ask for promotional waivers in mid-2025.

- Review tenure flexibility—longer tenures lower your EMI but increase total interest.

Expert Insight

In 2025, some state-by-state subsidies (like in Delhi, Maharashtra, Gujarat) are only available if you opt for financing by recognized banks or NBFCs. Check local government portals for lender tie-ups.

When Should You Apply for an EV Loan? (Best Timing for Indian Buyers)

Timing matters when applying for EV loans in India. Here’s what you should know:

- Apply just after banks/NBFCs announce rate reductions or festival offers (Independence Day, Dussehra, Diwali).

- If you’re buying a newly launched EV, banks often offer “introductory” low-rate offers for 2-3 months.

- Many lenders roll out EV-specific cashback or subsidy-linked schemes mid-year (July-September 2025).

- End of the financial year (March 2025) is also ideal, as banks want to meet loan targets.

- Check if state-level EV incentives have new budget allocations (often April or October).

- Avoid peak months (January, May) when demand—and rates—may be higher due to school admissions or holiday buying.

Did You Know?

In June 2025, Maharashtra renewed its EV subsidy scheme, with banks partnering for on-the-spot loan approval at official dealerships for eligible buyers.

How to Use an EV EMI Calculator Step-By-Step?

Using an EV EMI calculator may sound complicated, but it’s straightforward. Here’s how you can do it within minutes:

- Visit the lender or manufacturer website that has the latest EMI calculator (e.g. Tata Motors, MG Motor, or SBI).

- Enter:

- Ex-showroom price (2025 updated)

- Your planned down payment

- Loan tenure (in months or years)

- Expected interest rate (check latest displayed)

- Some calculators let you add-on:

- Processing fee

- Extended warranty or insurance premiums

- Click “Calculate” or “Get EMI”.

- View your customized EMI, total repayment, and a detailed schedule of payments.

- Adjust your down payment or tenure to see real-time impact on EMI and interest costs.

Example for Ola S1 Pro Scooter (2025 Price)

- Ex-showroom: ₹1,29,999

- Down payment: ₹30,000

- Tenure: 5 years

- Interest Rate: 9.25%

- Processing fee: ₹4000

Calculated EMI: ₹2,161/month

Total Interest Cost: ₹20,689

Total Repayment: ₹1,54,689

Expert Insight

Always factor in RTO registration charges and insurance premiums, which can increase the loan amount (and EMI) if you opt for 100% financing.

What Factors Affect Your EV EMI Amount in 2025?

You may notice EMI amounts vary even for the same vehicle. Several factors play a role:

- Vehicle Price: Higher the cost, more the loan and EMI.

- Down Payment: Bigger upfront payment = Lower EMI.

- Loan Tenure: More years = Smaller monthly EMI, but higher total interest.

- Interest Rate: Varies by lender, credit score, and EV model.

- Insurance, Accessories: If clubbed with loan, raises EMI.

- Processing Fees & Add-ons: Some banks let you roll these into the loan.

Important Points

- Manufacturer tie-ups can get you lower rates (e.g. Tata Capital for Tata EVs).

- State or central EV subsidies, if availed, will reduce effective amount you need to borrow.

- If you have a good credit score (above 750), some banks offer “special low” EMI for EV loans in 2025.

How Much EMI Will You Pay For Top Electric Cars and Bikes in 2025?

Choosing a model? Here’s a comparison of EMIs for the top-selling electric vehicles in India in 2025, calculated with average market rates:

| Model | Ex-showroom Price | Down Payment (20%) | Loan (80%) | Avg. Interest Rate (2025) | Tenure (Years) | EMI (₹/month) |

|---|---|---|---|---|---|---|

| Tata Nexon EV LR | ₹16,99,000 | ₹3,39,800 | ₹13,59,200 | 8.75% | 7 | ₹23,236 |

| Tata Tiago EV XZ+ | ₹9,89,000 | ₹1,97,800 | ₹7,91,200 | 8.60% | 7 | ₹13,521 |

| MG ZS EV Smart | ₹18,98,000 | ₹3,79,600 | ₹15,18,400 | 8.90% | 7 | ₹25,658 |

| Mahindra XUV400 EL | ₹17,49,000 | ₹3,49,800 | ₹13,99,200 | 8.75% | 7 | ₹23,854 |

| Hyundai Kona EV | ₹23,84,000 | ₹4,76,800 | ₹19,07,200 | 8.60% | 7 | ₹32,589 |

| Ola S1 Pro Gen 2 | ₹1,29,999 | ₹26,000 | ₹1,03,999 | 9.25% | 5 | ₹1,736 |

| Ather 450X Gen 4 | ₹1,45,000 | ₹29,000 | ₹1,16,000 | 9.15% | 5 | ₹1,887 |

| TVS iQube ST | ₹1,38,000 | ₹27,600 | ₹1,10,400 | 9.25% | 5 | ₹1,811 |

| Bajaj Chetak Premium | ₹1,43,000 | ₹28,600 | ₹1,14,400 | 9.10% | 5 | ₹1,873 |

| Hero Vida V1 Pro | ₹1,25,000 | ₹25,000 | ₹1,00,000 | 9.30% | 5 | ₹1,697 |

What This Means for You

- You can pick an EMI that’s comfortable to your monthly budget.

- Two-wheeler EMIs now start under ₹2,000/month, making EV scooters very affordable if you need daily commute savings.

- Most cars, especially Tata and Mahindra EVs, are packaged with loan schemes by their own finance arms for better rates.

Did You Know?

According to FADA, over 56% of new electric two-wheelers and 61% of electric cars sold in the first half of 2025 in India were bought with bank finance and calculated via EMI calculators.

Which is Better: Bank vs NBFC vs OEM Finance for EVs in 2025?

Choosing the right lender for your electric vehicle can save you money and hassle. Here’s how they all stack up:

Banks (Public/Private):

- Pro: Lower base interest rates, flexible tenure, more transparency.

- Pro: National reach, eligible for state EV interest subventions.

- Con: Longer approval process, stricter eligibility.

NBFCs:

- Pro: Quick approval, flexible documentation, more open to self-employed/first-time borrowers.

- Pro: Often bundled with dealer offers for two-wheelers.

- Con: Slightly higher rates, add-ons can hike up EMI if not careful.

OEM/Affiliate Finance (e.g., Tata Capital, Mahindra Finance):

- Pro: Model-specific low or zero interest for launch, quick processing at dealership.

- Pro: Waivers and bundled discounts (insurance, maintenance packs).

- Con: May have tie-in requirements to buy from select dealers.

How You Can Decide

- Seek bank finance if you have a high CIBIL score and want maximum transparency.

- Choose NBFCs if speed or flexible paperwork is key (good for young professionals, gig workers).

- Go for OEM finance if exclusive offers tempt you or you want bundled peace-of-mind.

Expert Insight

In 2025, Tata Motors’ in-house finance covers up to 100% on-road price for Nexon and Tiago EVs, with processing fees as low as ₹1,999—much lower than major banks!

What Subsidies, Tax Benefits, and Government Schemes Affect EV Loan EMIs?

Indian government realizes the cost barrier for EVs, so it supports buyers through various 2025 schemes:

- Central FAME-II subsidy: Direct cash benefit up to ₹1.5 lakh for eligible four-wheelers & up to ₹20,000 for two-wheelers, reducing upfront cost—and thus your loan/EMI.

- Section 80EEB Tax Relief: You can claim up to ₹1.5 lakh interest deduction per year on your EV loan EMI (for buyers until March 31, 2025).

- State-Level Schemes: Delhi, Maharashtra, Gujarat, Karnataka, and others provide extra subsidies, road tax waivers, or registration charge relief.

- Scrappage scheme: Exchanging your old petrol/diesel vehicle may get you extra cash off, lowering your EMI burden even more.

For Example

- Maharashtra EV buyers can avail up to ₹1 lakh for certain new electric cars, over and above central schemes.

- Delhi waives road tax and registration (worth ₹1-3 lakh for many cars in 2025).

Did You Know?

If your EV loan is availed from a scheduled bank or NBFC, you can claim tax benefits on the interest paid under Section 80EEB until 2025—double-check with your CA for optimum saving!

How Do Real Indian Buyers Use EV EMI Calculators? (Case Studies & Experiences)

User stories highlight how practical these tools are. Here are real first-hand accounts from 2025:

Case Study 1: Sangeeta, Bengaluru

- Wanted a Tata Tiago EV for her daily commute.

- Used three different EMI calculators (SBI, Tata Motors, Bank of Baroda) to compare EMIs.

- Adjusted tenure from 5 to 7 years to see the best EMI for her salary.

- Ended up choosing Tata Capital due to special 0.5% lower rate for Tata EVs.

- Saved over ₹22,000 in total interest over 7 years compared to a regular auto loan!

Case Study 2: Rakesh, Pune

- Shortlisted Ola S1 Pro and Ather 450X, worried about hidden charges.

- Online EMI calculator factored in registration and insurance.

- Opted for a slightly higher down payment to reduce EMI below ₹2,000/month.

- Used the EMI schedule to check loan closure flexibility.

- Loan sanctioned in 2 hours at dealer itself, thanks to NBFC instant-approval process.

Case Study 3: Anita, Delhi

- Replaced her old petrol Maruti with a MG ZS EV.

- Compared EMI options from HDFC, ICICI, and Mahindra Finance; factored in central/states subsidies.

- Used FAME-II, Delhi subsidy, and road tax waiver to reduce overall EMI burden.

- Found EMI calculator’s loan amortization chart handy to plan for early repayment in year 3.

Expert Insight

User research in early 2025 found that over 75% of Indian EV buyers now use at least one EMI calculator before finalizing their loan or down payment details.

Why is the EV EMI Calculator Important for Your Financial Planning?

Electric cars and scooters are a long-term investment, and EMIs can last years. Proper planning means:

- No nasty surprises months later if your budget shifts.

- Quick comparison for multiple models, variants, and offers.

- Customization: Adjust tenure and down payment as you like.

- Understanding if you should buy now or wait for subsidies/schemes later in 2025.

Common Benefits in India

- Reduces financial anxiety, especially for first-time EV buyers.

- Handy for families pooling finances for a single vehicle.

- Compatible with latest 2025 bank rates, incentives, and loan deals—so accuracy is high.

If you are risk-averse or conservative financially, you can pick a longer tenure or a higher initial down payment to keep EMIs manageable.

Did You Know?

More than 40% of new EV buyers in 2025 book vehicles online from their phones—using EMI calculators from their apps, without ever stepping into a bank!

How Can You Get the Lowest EMI for Your EV in 2025?

If you want the cheapest EMI for your electric car or bike, here are some clear practical steps:

- Increase your down payment—EMI drops sharply if you pay 30-40% upfront.

- Choose the longest repayment tenure you’re comfortable with (max 7 years is standard in 2025).

- Always compare at least 3 bank/NBFC offers side-by-side.

- Look for special reduced-rate festivals (Diwali, Independence Day, manufacturer “Green” schemes).

- Use manufacturer or state subsidies to bring down loan value.

- Max out Section 80EEB tax deduction for interest paid (till the scheme lasts).

- Beware of very low EMI “teaser” offers that balloon later—read all terms carefully.

Example

- If your EMI for a Tata Nexon EV is ₹24,000 over 5 years, increasing tenure to 7 years or paying a higher down payment can cut your EMI to ₹17,000-19,000/month.

You can easily test all combinations in an EMI calculator, then decide what fits your family’s monthly income.

Expert Insight

Public sector banks sometimes offer the lowest rates for women EV buyers or first-time vehicle owners—check for special schemes in 2025!

Conclusion

An EV EMI calculator is your smartest tool for planning an electric vehicle purchase in India. By giving you instant, accurate EMI details based on latest 2025 prices, loan rates, and your own preferences, it puts you in full control. You can:

- Plan your expenses realistically.

- Compare car and bike models, lenders, and EMI scenarios side by side.

- Use state and central government benefits, so your total loan—and interest burden—drops.

- Avoid surprises from hidden charges or fluctuating schemes.

Whether you are a salaried professional in Mumbai, a student in Bengaluru, or a family buyer in Delhi, using an EV EMI calculator will help you make the most informed, risk-free, and satisfying EV buying decision.

Take Action: Always use a trusted EV EMI calculator before applying for your loan. Compare at least three offers, factor in all subsidies, and customize EMI amounts based on your actual financial comfort. This one step can save you lakhs over the lifetime of your EV purchase!

FAQs

1. Is the EV EMI calculator free to use?

Yes, all leading banks and auto OEM EMI calculators are free, and you can use them as many times as you need.

2. Can I trust the EMI shown by the calculator for my final loan?

Generally yes, but the final EMI may vary slightly due to add-ons like insurance or last-minute fee changes by the lender. Always confirm details before signing an agreement.

3. Does the EMI calculator include state and central subsidies?

Most calculators now let you add government/central or state subsidies for an accurate estimate, but check with the portal if you are eligible for these.

4. Is my credit score checked during EMI calculator usage?

No, calculators don’t check your credit score—you enter the interest rate shown on bank websites based on your likely eligibility.

5. Can I prepay my EV loan early? Will the calculator show this impact?

You can prepay, but calculators usually show only EMIs for the original term. Check with your bank/NBFC for pre-payment penalties or benefits, and adjust your planning accordingly.

Disclaimer: The information in this article, including prices and rates, is based on the latest 2025 Indian market data available as of date of writing. Always confirm details with your lender, manufacturer, and local state authorities before making financial commitments. Government policies and offers can change rapidly, so review details before applying.